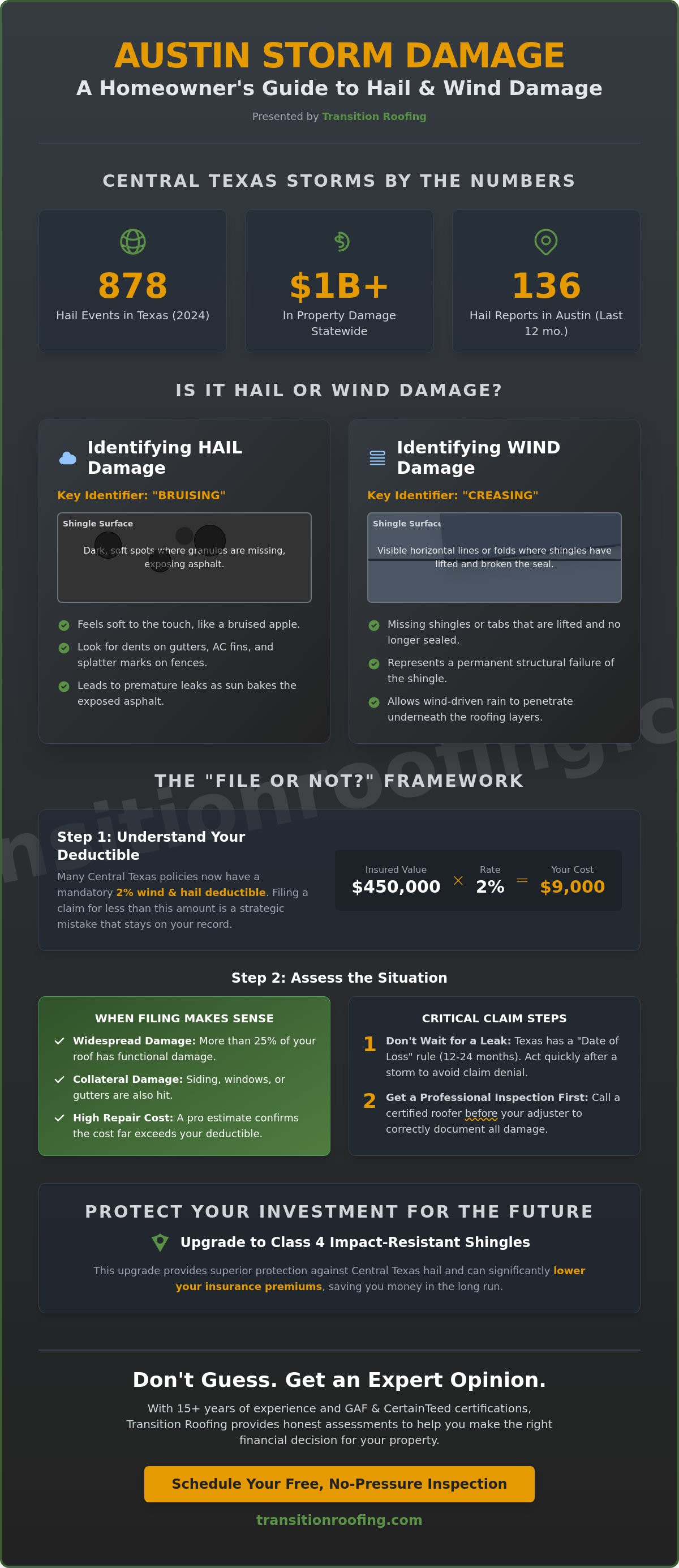

Texas experienced 878 individual hail events in 2024 alone, resulting in over $1 billion in property damage across the state. In Austin, TX, our neighborhoods faced 136 on-the-ground hail reports in the last 12 months, leaving many homeowners staring at their shingles and asking, “Is this hail or wind damage and should I file an insurance claim?” It is a valid concern, especially with the 2026 insurance updates that shifted many Central Texas policies to a mandatory 2% deductible. You should not have to guess if a storm actually compromised your roof or if you are just seeing normal aging.

We understand the stress of dealing with aggressive door-to-door contractors and the fear of your insurance premiums spiking. With over 15 years of experience and certifications from GAF and CertainTeed, we believe in providing honest answers rather than high-pressure sales pitches. This guide will help you accurately identify storm damage on your Central Texas roof and decide if filing an insurance claim is the right financial move for your property. We will break down the physical signs of wind versus hail and provide a clear framework for when to call your adjuster and when to wait.

Key Takeaways

- Learn the visual differences between hail “bruising” and wind-induced “creasing” to know exactly what to look for after a storm.

- Use our professional financial framework to answer the question: Is this hail or wind damage and should I file an insurance claim?

- Understand the Texas “Date of Loss” rule and why waiting for a leak can disqualify you from an insurance-funded replacement.

- Discover the two critical steps to take before calling your adjuster to ensure your claim is documented correctly from the start.

- Find out how upgrading to Class 4 impact-resistant shingles can lower your premiums and provide long-term protection in the Central Texas climate.

Identifying Hail vs. Wind Damage on Your Austin, TX Roof

Most Austin homeowners walk their property perimeter after a storm, but looking up from the driveway rarely reveals the full truth. To understand the risks, you first need to know what hail is and how it interacts with different roofing materials. You might be asking yourself, “Is this hail or wind damage and should I file an insurance claim?” but the answer usually hides in the details only visible from the ridge line. Ground-level inspections are often misleading because shingle “bruising” is invisible from 20 feet below, and high-wind creases can be hidden by the shingles above them.

To better understand this concept, watch this helpful video:

Under Texas insurance standards, functional damage is defined as a storm-related loss that compromises the roof’s water-shedding ability or expected service life, while cosmetic damage is a purely aesthetic change that does not impact performance. Because the City of Austin requires a building permit for any repair covering more than 20% of the roof area, identifying functional damage early is critical for staying within local codes. If you are unsure about the state of your shingles, a professional roof inspection is the most reliable way to document these issues for your carrier.

Visual Cues for Hail Impact

Hail damage appears as “bruising” on the shingle surface. These are dark, soft spots where the protective granules have been knocked away by ice impact, exposing the underlying asphalt. Before climbing a ladder, check for “splatter marks” on wooden fences or circular dents in soft metals like gutters, downspouts, and AC fins. On the shingles, these impact points often feel soft to the touch, similar to the skin of a bruised apple. If these spots are left unaddressed, the Texas sun will bake the exposed asphalt, leading to premature leaks and shingle failure.

Signs of High-Wind Stress

Wind damage is characterized by “creased” shingles, where high gusts lift the shingle and break the internal fiberglass matting. You may identify missing shingles or tabs that are “tabbed up” but not completely detached. Look for horizontal lines across the top of the shingles where they have folded back during gusts. These creases are permanent structural failures that prevent the shingle from sealing properly again. Even if the shingle looks flat now, a broken seal allows rain to blow underneath the material during the next Central Texas storm cycle.

The ‘File or Not?’ Framework for Austin TX Property Owners

Deciding whether to open a claim involves more than just seeing spots on your shingles. In 2026, the standard wind and hail deductible for a home in Austin TX is 2% of the insured dwelling value. If your home is insured for $450,000, your out-of-pocket cost is $9,000 before the insurance company pays a dime. Before you ask, “Is this hail or wind damage and should I file an insurance claim?” you need to know if the total repair cost actually clears that hurdle. Filing a claim that pays out less than your deductible is a strategic mistake that stays on your insurance history for years.

Texas policyholders generally have between 12 and 24 months to report a loss. This “Date of Loss” rule means you can’t ignore a storm today and try to claim it when you notice a leak three years later. We recommend a professional inspection from Transition Roofing to document the specific event date and damage severity. When identifying hail damage, adjusters look for a specific density of hits within a “test square.” If you’re seeing this on your roof, we can take a look and give you a clear plan to ensure you don’t file a claim that ends in a denial.

When Filing a Claim Makes Sense

- If functional damage covers more than 25% of your roof, the cost of a full replacement will far exceed your 2% deductible.

- When a storm leaves collateral damage on your siding, windows, and gutters, the combined total often justifies the claim.

- If your roof is less than 10 years old and has significant hail bruising, a replacement protects your long term property value.

When to Consider Paying Out-of-Pocket

- Small repairs, like replacing a few wind-blown shingles, usually cost less than $1,000 and should be handled privately.

- Adjusters often deny claims for roofs with pre-existing “maintenance neglect” or simple granule loss from old age.

- If your deductible is higher than the estimated repair, paying out-of-pocket keeps your insurance history clean and prevents potential premium hikes.

Navigating the Texas Insurance Claim Process in Austin, TX

Filing a claim in the Central Texas climate requires a methodical approach to ensure you don’t leave money on the table. Once you have identified potential issues, follow these four steps to protect your property. First, document the storm date and take ground-level photos of hail stones or downed debris. Second, schedule a roof inspection in Austin with a certified contractor to verify the damage. Third, notify your insurance carrier to start the claim and receive your claim number. Finally, ensure your contractor is present during the adjuster’s visit to point out hidden damage that a quick walk-through might miss.

Under Texas Insurance Code Chapter 542, insurance companies must acknowledge receipt of your claim within 15 days and begin their investigation. When you ask, “Is this hail or wind damage and should I file an insurance claim?” having an expert by your side during the adjuster’s walk-through provides the best chance at a fair outcome. We provide the technical documentation adjusters need to justify a full replacement rather than a simple patch job.

Understanding the Texas Deductible Law

It is strictly illegal for a contractor to “waive” or “absorb” your deductible in Texas. This law was reinforced to prevent insurance fraud and ensure high standards of repair. If a contractor offers to cover your deductible, they’re asking you to participate in a Class A misdemeanor. For a typical Austin home with a 2% deductible on a $400,000 policy, you are legally required to pay that $8,000 out of pocket. We provide transparent invoicing to ensure you remain in full compliance with state regulations.

The Role of the Adjuster vs. The Contractor

Adjusters often work under high-volume pressure and may miss subtle signs of fiberglass matting failure. A commercial roofing expert uses specialized tools to catch what a standard adjuster’s visual check misses. If you receive a “partial” approval for only one slope of your roof, your contractor can provide a “supplement” request. This is a formal document showing why the entire roof requires replacement to maintain structural integrity. If you’re dealing with a confusing claim, schedule a roof inspection in Austin today so we can give you a clear plan.

Protecting Your Austin TX Property from Future Storm Damage

The relentless heat in Central Texas accelerates shingle aging. When summer temperatures exceed 100 degrees for weeks at a time, the asphalt in your shingles loses its essential oils and becomes brittle. This thermal stress means a roof that survived a storm three years ago might shatter during the next hail event. If you’re currently asking, “Is this hail or wind damage and should I file an insurance claim?” it’s a strategic time to consider materials that handle these cycles better. Upgrading to Class 4 Impact Resistant shingles is a proven way to secure your home. In Texas, these high-performance shingles often qualify for insurance premium discounts between 15% and 35%.

Residential Storm Resilience in Austin TX

- GAF and Certainteed high-wind rated shingle systems are engineered to withstand gusts up to 130 mph, which is vital for the intense spring supercells we see in the area.

- Metal roofing systems are increasingly popular because they don’t become brittle with age and offer the highest level of fire and impact resistance.

- Choosing impact-resistant materials is a long-term investment that increases property value while lowering your annual cost of ownership.

Commercial Storm Preparedness

For business owners, the stakes of a storm are even higher. We highly recommend preventative maintenance programs to catch drainage issues before they lead to structural weight problems. After a major hail event, TPO and PVC membranes require professional inspections to check for micro-fractures. These tiny cracks allow moisture to seep into the insulation board, which can rot the deck from the inside out. Keeping detailed maintenance records is also essential for ensuring your commercial roof warranty stays valid after a major weather event.

Don’t let the promise of a “free” roof from a door-to-door storm chaser turn into a structural or legal nightmare. These high-pressure sales tactics often lead to cut corners and ignored building codes. If you’re dealing with potential storm damage, we can take a look and give you a clear plan. Schedule a roof inspection in Austin today to ensure your property is truly protected for the long haul.

Secure Your Austin TX Property with Professional Storm Guidance

Navigating the complex world of insurance claims after a Central Texas storm shouldn’t be a solitary burden. We’ve explored the physical differences in shingle failure and the strict legalities of the Texas deductible laws. Now, the final step is moving your property from a state of vulnerability to one of total security. Whether you are dealing with a residential shingle system or a commercial flat roof, the goal is long-term protection rather than a temporary patch job. If you are still asking yourself, “Is this hail or wind damage and should I file an insurance claim?” the answer lies in a detailed, professional assessment that looks beyond the surface.

Transition Roofing brings over 15 years of local expertise to every project. As GAF and Certainteed Master Shingle Applicators with an A+ BBB rating, we pride ourselves on being the trusted protector for our neighbors. We don’t just fix roofs; we manage the transition to ensure your investment is built to last against the next round of Texas weather. If you’re dealing with storm damage, we can take a look and give you a clear plan today. Let’s ensure your home remains a safe haven for years to come.

Common Questions About Austin Storm Damage Claims

How long do I have to file a hail damage claim in Texas?

You typically have 12 to 24 months to file a claim from the specific “Date of Loss.” While Texas law allows for a two year statute of limitations on lawsuits, most residential policies require you to report the damage within 365 days to qualify for full Replacement Cost Value. Waiting too long can lead to a denial because it becomes difficult to prove which specific storm caused the bruising versus normal wear and tear.

Will my insurance premiums go up if I file a roof claim after a storm?

Filing a single claim for an “Act of God” event like a hailstorm generally does not cause your individual premiums to spike. However, insurance companies often raise rates for an entire zip code in Austin, TX after a major weather event. Since your rates may go up regardless of whether you file, it’s often better to have a secure, new roof paid for by the carrier than to pay higher premiums for a damaged one.

Can I be dropped by my insurance for filing a weather-related claim in Austin?

No, Texas insurance companies are prohibited from non-renewing your policy solely because you filed a single claim for weather-related damage. Under HB 2067, which took effect January 1, 2026, carriers must provide a written explanation for any canceled or non-renewed policies. This protection ensures you can address your question—is this hail or wind damage and should I file an insurance claim?—without the fear of losing your coverage immediately.

What happens if my insurance adjuster denies my claim but my contractor sees damage?

You have the right to request a second inspection or enter the “appraisal” process if there’s a disagreement. Adjusters often work under tight schedules and may overlook subtle signs of fiberglass matting failure. We can meet a different adjuster on-site to provide a side-by-side comparison of the damage. Providing high-resolution photos of collateral damage on gutters and AC units often helps reverse a denial during the supplement process.

Is it worth filing a claim for just a few missing shingles?

It’s rarely worth filing a claim for minor shingle displacement because the repair cost is often less than your 2% deductible. For an Austin home with a $400,000 dwelling value, your $8,000 deductible far exceeds the cost of a $500 shingle patch. However, you should still get a professional inspection to see if those missing shingles are part of a larger pattern of wind-induced creasing that justifies a full replacement.